Investment Markets in Review – Q1 2023

Pitcher Partners Wealth Management (Brisbane) | The information in this article is current as at 5 April 2023.

Despite growing recession risks, most asset classes rallied strongly over the March quarter although the headline performance numbers masked some considerable volatility intra-quarter, especially within fixed income markets.

As anticipated, headline inflationary pressures globally are beginning to ease, whilst activity levels of many major economies have proven to be far more resilient to the record level of financial tightening in the past 12-18 months than originally forecast. During January and February, hopes were raised of a soft economic landing and avoiding recession, especially given the re-opening of China’s economy. However, these hopes have been somewhat dashed by the first major cracks appearing in the financial system since central banks began lifting rates last year. We witnessed the collapse of US regional banks Silicon Valley Bank and Signature Bank, coupled with stresses across a number of other firms as well. Credit Suisse, a ~170yr old Globally Systemic Important Bank, which was already battling its own challenges amid its major restructuring program, was ultimately forced by the Swiss central bank to be acquired by UBS.

These events echoed memories of the Global Financial Crisis (GFC) in 2008. We witnessed these views manifest themselves most clearly through the fixed income markets, where wild daily price swings (especially in the 2yr part of the US yield curve) eclipsed even those seen in the GFC.

Expectations of further rate hikes required to address sticky services inflation were reversed swiftly, repricing to the view that several rate cuts were needed to kickstart economies heading into recession – priced in for the second half of this year.

Late in the quarter, in response to the declining oil price, OPEC announced a significant cut to production targets which have at the time of writing, reignited concerns over an additional wave of inflationary pressures, especially toward Europe which remains on a fragile path to recovery.

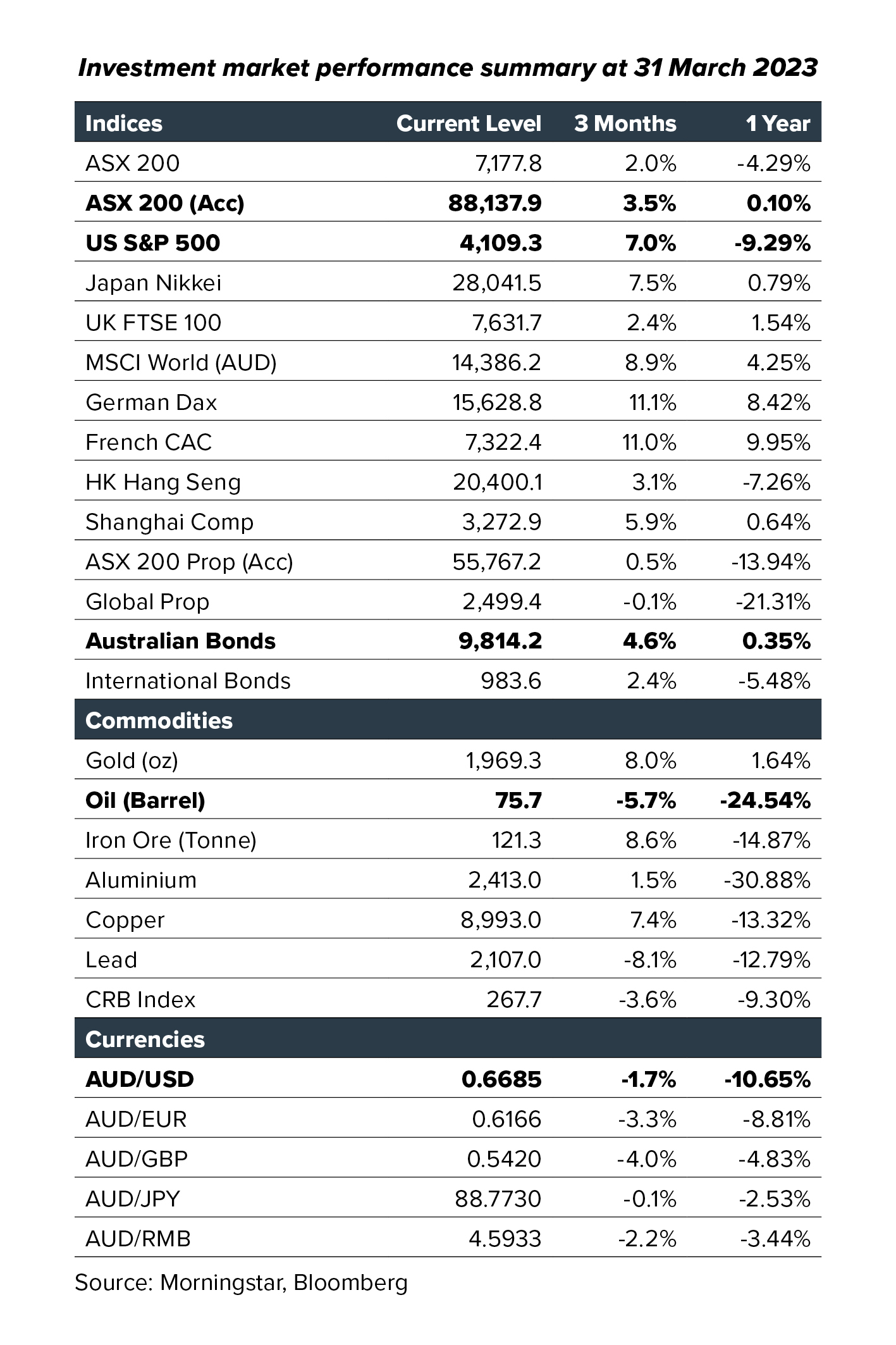

We now provide some key comments regarding the performance of the major asset classes in the March quarter as below;

Shrugging off pressures within the financial sector, Global equities outperformed our local share market handsomely over the period, as investors were buoyed over potentially having hit peak interest rate levels.

On a regional basis, Europe was the strongest performing region, followed by the US and Japan. The exuberance around China’s re-opening of its economy post COVID was tempered late in the quarter and was the main factor for why emerging markets lagged developed markets.

Growth investors outperformed value significantly given the weakness within the financials and energy sectors. This resulted in the consumer discretionary, communication and technology sectors to outperform sharply, although we note the gains were concentrated in just a handful of mega-cap companies.

Locally, the 1H23 reporting season highlighted that Australian listed companies continue to benefit from strong demand. Cost pressures continued to weigh on profit margins, with many companies struggling to pass these expenses through to consumers. Large caps continued their strong run of outperformance versus small caps, while at the sector level, banks, utilities and energy lagged. Leading sectors were consumer businesses, technology and materials.

In turning towards fixed income, despite both the Federal Reserve and the RBA continuing to lift cash rates through the quarter, both local and offshore fixed income markets rallied strongly. As highlighted previously, the sharp swing in expectations from rate hikes to rate cuts in 2H23, generated a welcome return in performance following double digit losses through 2022. Central bank guidance continues to paint a slightly more bearish/hawkish stance than where the money markets are positioned.

In credit markets, the Swiss National Bank’s decision to write off the entire ~US$17bn Tier 1 capital of Credit Suisse created some turmoil within the AT1 sector of US and European hybrid securities (and equivalents). Australian hybrids were not immune from the volatility but outperformed in comparison, reflecting the relative strength and confidence in our banking sector (and underlying terms of the securities themselves). We witnessed some widening in spreads over increasing recessionary risks but these losses were more than offset by gains through rate duration.

Listed property markets lagged the advance of broader equity markets, with both our local and global REIT benchmarks producing small positive returns. While investors have been attracted to the valuation dispersion on offer between listed and unlisted investments, the turbulence within the US regional banks, a key source of funding for parts of the unlisted property sector, prompted valuation concerns specifically around the commercial real estate sector and weighed on overall sentiment to this asset class.

We witnessed a wide dispersion in the return of various commodities – the reopening trade of China’s economy boosted the likes of Copper and Iron Ore, Oil fell 6% before rallying on the news of impending production cuts from OPEC. Gold rallied strongly to close near US$2,000 per oz.

The Australian dollar weakened slightly against the US dollar over the period, to close the quarter at $0.6685.

In our diverse mix of articles this quarter, we discuss the very topical issue of Carbon Capture & Storage technology, a key solution for many heavy carbon emitters in being able to achieve a sustainable carbon reduction strategy.

We also provide an introduction and overview of Managed Futures, a really interesting investment strategy which is based upon trend following and could help provide additional diversification benefits to investment portfolio