Business Radar 2025 Understanding the businesses that drive Australia's economy

The Business Radar report canvasses the trends, challenges and opportunities experienced by Australia’s middle market businesses.

Independently commissioned, our most recent survey captured the sentiment of nearly 150 owners and leaders across a range of growth stages, states and industries.

Here, you’ll read how business leaders feel about the current and future success of their businesses and what that could indicate for Australia’s economy.

Key findings

- AI adoption is widespread but strategic implementation lags: While 93% of leaders are familiar with AI and 72% actively use AI tools, only 13% have made it a true strategic priority with dedicated budgets and scaling plans

- Workforce transformation is underway with mixed impacts: Half of businesses report moderate role changes, with employees spending more time on creative work (42%) and less on administrative tasks (36%), though concerns about job losses have increased from 29% to 37% since 2023

- It’s only just the beginning for AI adoption: Growth-stage businesses (63%) and those with 100-250 employees (61%) show highest readiness for AI-driven industry shifts, and middle market businesses in the growth phase are incorporating operational advantages through bold AI implementation

- Middle market confidence remains stable despite AI disruption concerns: Though mature businesses show declining confidence as they view their size and legacy as potential disadvantages in AI transformation

Read on to learn how middle market leaders are successfully navigating the AI transformation and the strategic actions you can take to position your business for the next generation of growth or download your copy of the latest Business Radar.

AI Integration: From novelty to normality

The readiness gap

More than half of businesses say they’re ready to adopt AI, but the foundations may not yet be in place. Only 12% feel fully prepared to scale adoption, while 39% are only fairly ready. Almost 35% report being neutral or partially ready, and 15% are somewhat unprepared or not ready at all.

The barriers are clear: technical and compliance issues (65%), capability gaps (64%), lack of trust in AI outputs (52%), financial constraints (46%) and cultural challenges (45%).

Business leaders should never assume AI outputs are completely accurate or trustworthy without verification. A healthy level of scepticism is valuable: question what AI produces, ask for evidence, and examine the assumptions behind its answers.

Main challenges to AI adoption

Key actions to take:

Build the base before adding AI Build strong data systems, governance and business intelligence capability before layering AI on top. Check your infrastructure is ready for the increased loading. |

Bring your people with you Address employee concerns openly and invest in upskilling so they can thrive alongside AI.. |

Start with the outcomes in mind Decide what you want AI to achieve so it drives strategy, not side projects. |

Consider safeguards and reduce exposure Put policies, safeguards and education in place to prevent careless or unsafe use of the AI tools. |

Define the human value only you provide Distinguish your business and protect your revenue through the human skills and insights AI can’t replicate. |

Educate, educate, educate Looks for ways to provide training in multiple formats and forums, continue to share knowledge on types of tasks where AI adds value. |

Research and trial Get access to the latest AI developments, whether that is in-house expertise or outside advisors. Then try them out. |

Business confidence

Technology advancement drives confidence surge

Technology advancement has emerged as a major driver of confidence, cited by 43% of leaders as a positive factor – a dramatic increase from just 12% since our last survey.

This represents one of the most significant shifts we’ve observed, positioning technology as one of the top five positive factors since early 2024.

Leadership during uncertain times

How are leaders navigating extra turbulence?

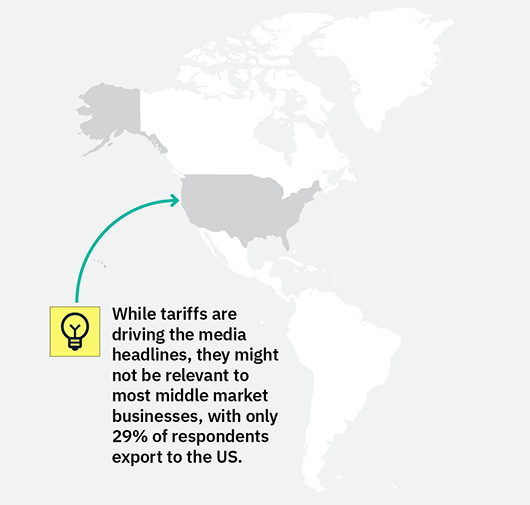

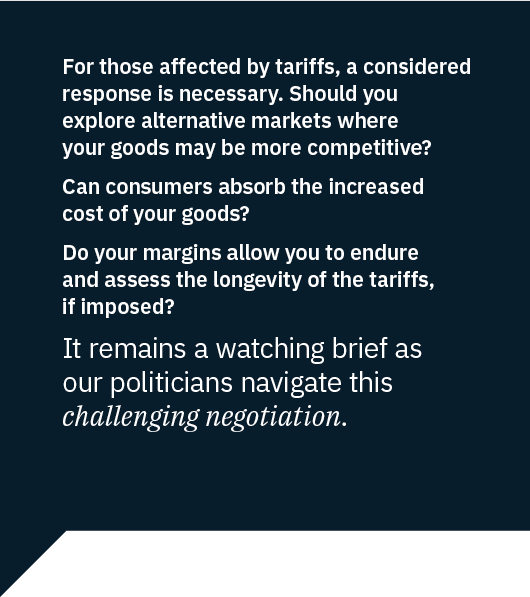

While the media reports would have us believe that business leaders are (very) afraid of an incoming catastrophe, our middle market business leaders aren’t panicking.

The vast majority – 83% – are seeing no or only moderate changes in uncertainty levels, with just 17% saying they’re facing high or extreme change, even in the face of tariffs, increasing global uncertainty, legislative change and disruptive technology.

These stats are reflected in on-the-ground observations

from Pitcher Partners’ experts.

“In the media, these are ‘uncertain times’, but clients are

more ‘steady as she goes’. Exporters have some concerns,

but they haven’t completely put the brakes on. We hear a lot

about catastrophe – but it hasn’t played out yet for many,”

said Chris Hanna, Principal, Pitcher Partners Adelaide.

Business’s change in uncertainty levels in light of recent events

Current business posture

Current risk appetite

Cutting costs, not quality

But what are leaders actually doing in response to the market uncertainty? When we dig deeper into business posture, an interesting tension emerges.

On one hand, 69% of respondents say they are actively looking to cut costs.

On the other, almost as many are pursuing growth initiatives – 67% are expanding into new markets and 65% are introducing new products and services.

This isn’t contradiction – it’s strategy.

Rather than choosing between caution and ambition, many middle market leaders are doing both. They’re taking a sophisticated and measured approach: optimising operations and cost structures to preserve margins, while simultaneously investing in areas that create long-term value. Two in five are focusing on supply chain and operational efficiency, and 40% have accelerated business model transformation – like investing in tech, digitising operations, etc.

It’s a sign that businesses are thinking broadly and taking actions on many important areas of their business: containing risk while preparing for opportunity.

In light of recent economic and market conditions, businesses have taken action on the following:

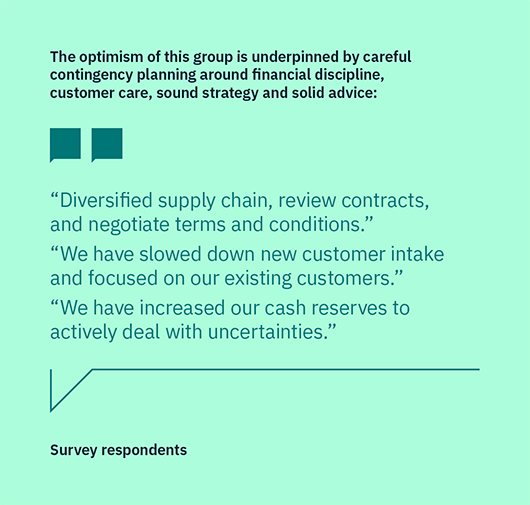

Confidence built on careful planning

To support this planning, businesses say they’re primarily seeking support from advisors or consultants (42%) or collaborating with industry groups and peers (44%).

Solid advice is always critical, but equally important are the strategic connections you forge. Great advisors will maintain and help you access their networks. Similarly, they should go beyond generalisations and instead listen, understand your unique context, and offer genuinely tailored solutions.

Key actions to take:

Balance cost cutting against growth Refine operations and supply chains to build efficiency while continuing to invest in innovation, expansion and customer value |

Strengthen your network Find mentors, organisations and advisors who connect you to wider networks and opportunities. |

Prioritise people Focus on strong, steady leadership that supports your team’s capability, motivation and stability. |

Make decisions based on strategy, not fear Get clear on your goals, and then hold your nerve. |

Build your buffers Whether that’s building a financial cushion or diversifying supply chains, customer base or revenue streams. |

Automation gives the edge Ensure your tech and AI are being used to re-skill your people and lift productivity |

Mandatory climate reporting and ESG

Awareness? Yes. Clarity? No.

Our respondents showed strong awareness of the incoming requirements, but many remain unclear on what it will actually mean for their businesses. Six in 10 say they have some level of familiarity with the new requirements, and more than half feel confident that they know what needs to happen to reach compliance. However, 75% say they’re not at all prepared or only somewhat prepared for mandatory climate reporting, despite the fast-approaching deadlines.

Extra work or business benefit?

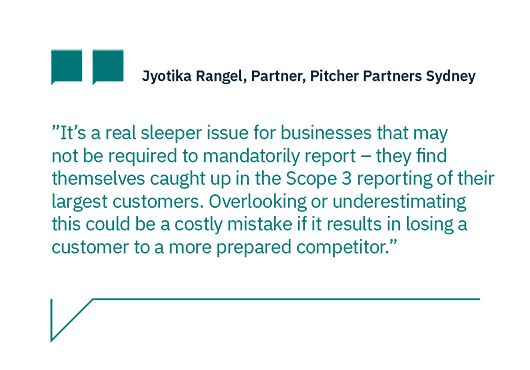

The middle market’s slower progress towards compliance could be linked to the perceived lack of value that the requirements add to their businesses. It’s clear that for many businesses, the reporting requirements are seen as an administrative burden.

Many middle market businesses are not likely to be caught in the reporting regime, unless required as part of the supply chain emissions reporting.

Turn the negative into a positive

Effective governance and strategic planning are crucial in meeting the new ESG and mandatory climate reporting requirements. By integrating these reporting requirements into the company’s governance framework, businesses can make sure that they are not only compliant but also strategically positioned to benefit from these regulations. This involves setting clear objectives, allocating resources efficiently, and continuously monitoring progress to meet the reporting standards.

Meet our middle market businesses

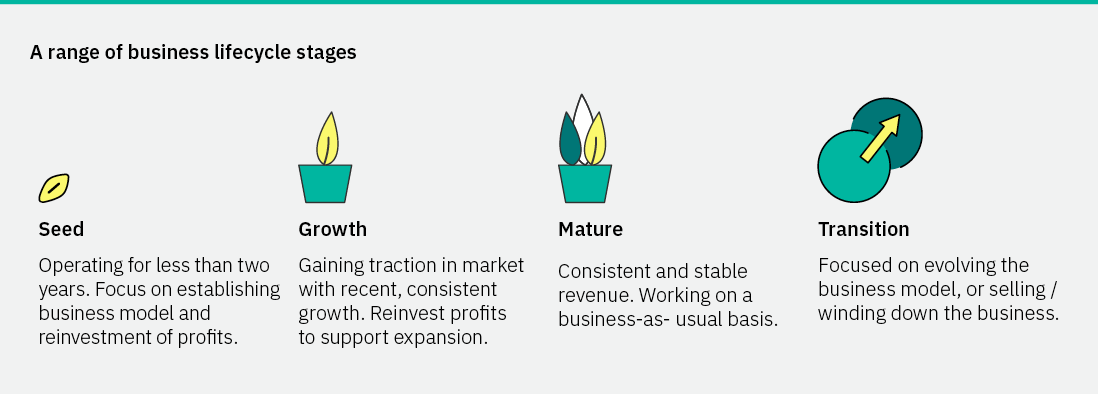

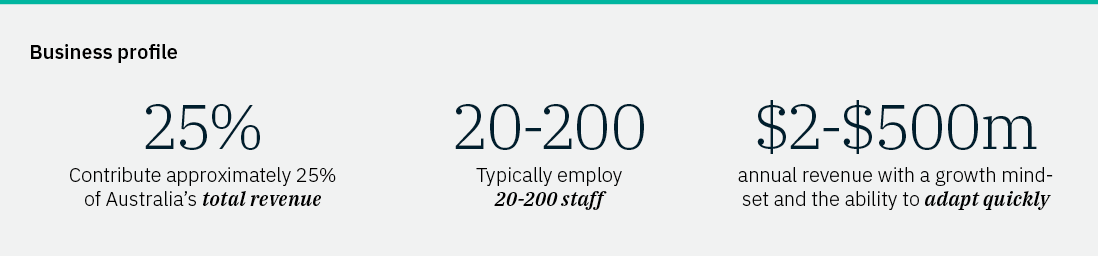

This report defines middle market businesses as typically employing 20–200 people with annual revenue of $2–$500 million. While their operating models, sizes and industries vary widely, these businesses can be categorised into four lifecycle stages.

Our experts